Insights | 16 Apr 2024

Ken Mulkearn | 05 Oct 2022

Which inflation measure: CPI, CPIH or RPI?

Official estimates of price inflation – which act as proxies for changes in the cost of living – remain an important input into wage-setting decisions. But users are often confused by the fact that the Office for National Statistics (ONS) publishes three different indicators: the ‘Consumer Prices Index’, or CPI; the ‘Consumer Prices Index including housing costs’, or CPIH, which is derived from the CPI and is the ONS’ headline measure; and the ‘Retail Prices Index’, or RPI, which, while it is no longer designated as a ‘national statistic’ by the ONS – for reasons which are disputed by many statisticians (more on which below) – continues to be published by the ONS and appears alongside the CPIH in its monthly detailed briefing note on consumer price inflation Consumer price inflation detailed briefing note - Office for National Statistics. (NB Further changes are afoot for the RPI, something we also look at in more detail below.)

So which one should you reference when it comes to deciding on annual pay rises? The difficulty here is that inflation is what’s known as a ‘latent variable’. This means that it cannot be observed directly and instead has to be inferred from mathematical formulas using sample data on prices as a main input. The different mathematical formulas involved in each of the official measures, as well as other differences, mean that there is not necessarily a single best measure for indicating how inflation might be taking place and the rate at which it might be increasing (or on rare occasions, falling). Issues include what items are included in the ‘basket’ of goods/services for measurement of price changes, and how the rate of change is calculated. While one measure might be said to overestimate the extent of inflation, yet another could be regarded as underestimating it. We consider each of the official measures in turn below.

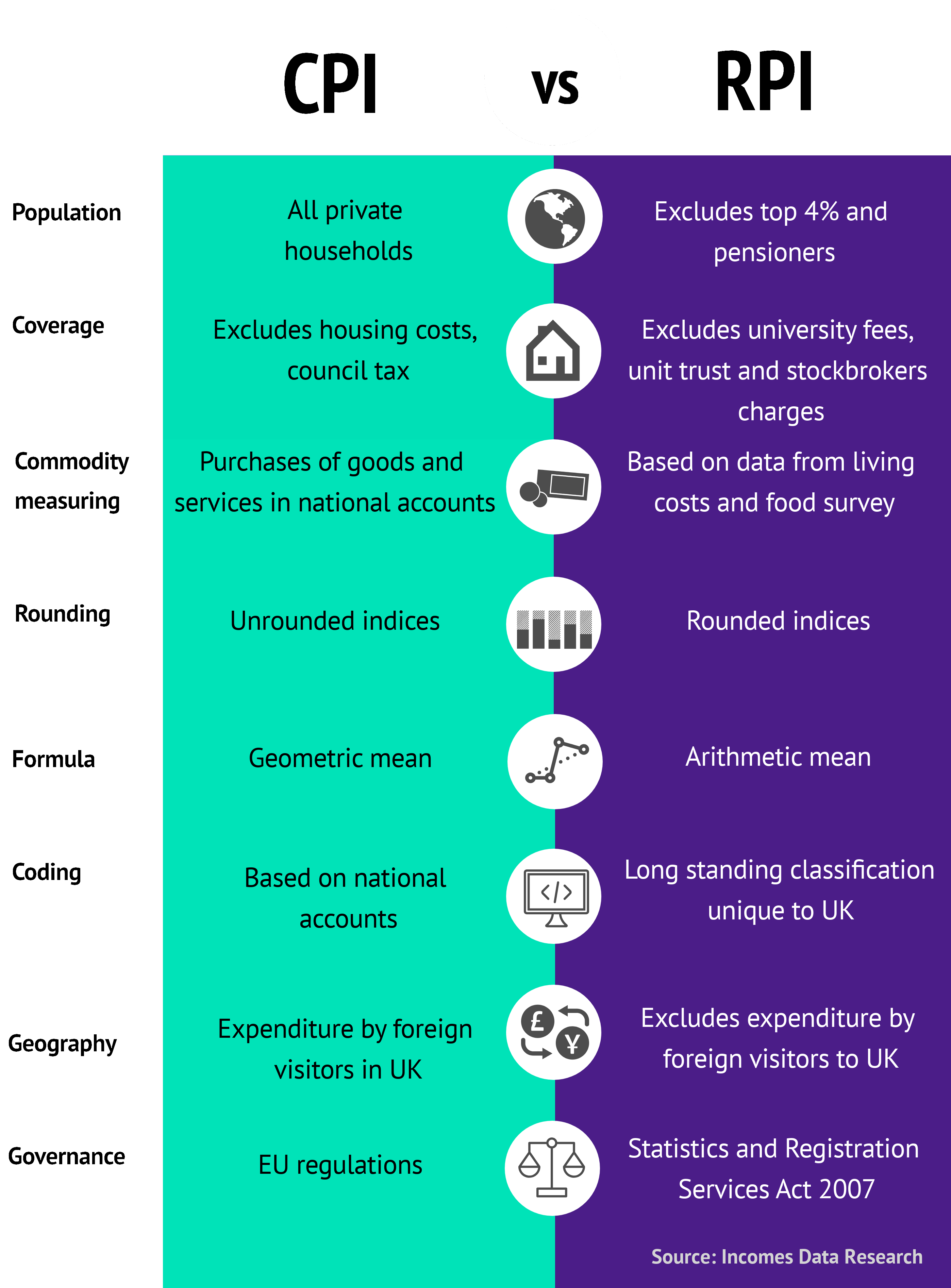

CPI – this is the Government’s main measure of inflation for macroeconomic management purposes, acting as it does as the inflation ‘target’ for the Bank of England in its interest rate-setting role. (This target is currently 2% and when inflation is significantly above or below this level the Bank’s Governor is required to write to the Treasury to explain what it is doing to try and get inflation back to the target level.) It was introduced comparatively recently, in 2003, apparently as a way of comparing inflation in the UK with inflation rates in other EU countries (its previous name – the Harmonised Index of Consumer Inflation, or HCIP – reflected this), though in fact most EU countries retain their own national consumer price indices as primary indicators of inflation and for uprating purposes. Its basket includes a number of items that are excluded from the RPI, for example university accommodation fees and foreign students’ tuition fees. But the main omission is housing costs, particularly in the form of mortgage interest payments, but also other items such as council tax. Since 2011 it has been used for the uprating of state benefits and as the measure of changes in prices element in the ‘triple lock’ mechanism for uprating basic state pensions; and since 2014 for personal tax allowances and thresholds. It calculates inflation mainly on the basis of the Jevons formula, using a geometric mean, which reduces the impact of large changes in the price of any particular element in the ‘basket’. The CPI tends to be the figure used by the media in their reporting of inflation, which, along with other factors – chiefly the fact that it is generally lower than the RPI, in a lengthy post-recession period when affordability has weighed heavier in the balance for employers – has made for a rise in its popularity as an indicator for pay-setting purposes; whether in fact it is suitable for this is something we consider below.

CPIH – this is the ONS’ headline measure of inflation in its monthly releases on the topic; the ‘H’ stands for housing. It was developed and launched in 2013 in response to the main shortcoming of its cousin the CPI, that it doesn’t include a measure of housing costs; the CPIH, by contrast, measures housing costs on the basis of rental equivalence – this means it uses the rent paid for an equivalent house as a proxy for an owner-occupier’s housing costs, and as such it does not capture house prices; it also calculates inflation mainly on the basis of the Jevons formula. Despite it being the ONS’ headline measure, it is largely ignored by the media in their reporting of inflation statistics; we’re not certain why this is the case, but it may be that journalists either don’t understand the differences between the various measures of inflation, do not wish to stray into a discussion of the differences or, given the CPI’s role in macroeconomic management, default to this as the seemingly sole indicator. The lack of media prominence may be a reason why, despite its inclusion of an estimate of housing costs, the CPIH is only rarely used as an inflation indicator for pay-setting purposes, though this could change.

RPI – this is the oldest measure of inflation, dating back to at least 1947. It is often referred to as the ‘all-items’ measure of inflation, since it aims to include a comprehensive list of areas of expenditure in its basket of goods and services; as such, it contains a number of items that are excluded from the CPI and CPIH, including council tax, mortgage interest payments, house depreciation, buildings insurance, ground rent and other house purchase costs such as estate agents’ and conveyancing fees. When it comes to calculating inflation, the RPI uses an equal combination of the Carli, Dutot and other formulas (see below); the ONS continues to publish the RPI but has said it is no longer a ‘national statistic’, mainly because the ONS considers that the Carli formula, which involves an arithmetic mean, leads it to overestimate inflation (we discuss this in more detail below). It continues to publish the RPI in part because of its role in uprating a long list of statutory items, including business tax rates, vehicle excise duty, fuel duty, duty on alcohol and tobacco, car and van fuel benefit and water charges; the RPI is also used for valuing index-linked Government bonds. The fact that it covers ‘all items’, especially house prices, and is used for uprating the list of items mentioned above are central explanations for the RPI’s continued prominent role in pay-setting.

There is an ongoing debate among statisticians about which measure of inflation is the best for measuring changes in the costs faced by households. A large part of this debate hinges on the different mathematical formulas used in the different measures of inflation. The House of Lords recently conducted an inquiry into the uses of RPI. One of the topics on which it heard evidence was the ‘formula effect’. This is the estimated difference between the CPI and RPI rates and is due to the different formulas used in each measure.

While the formulas are not the only reason for the difference in the rates shown by the two measures, they are often the largest element in a gap that has generally been in one direction – with the CPI consistently lower than the RPI. This is partly to do with the different types of arithmetical means used in each of the formulas. In addition, a recent methodological change by the ONS produced a widening of the gap. This change was the broadening of the range of clothing for which prices were collected. This produced price data that, when combined with the Carli formula, led to a significant increase in the annual rate of growth of the RPI. This had the effect of somewhat discrediting the RPI, particularly, it would appear, in the opinion of the ONS, who made the change that produced the increase. But it has had real effects, since a number of important items continue to be uprated using the RPI, with a consequent impact on consumers.

However, the debate over the suitability of the different indices has continued, since many users of the RPI feel it to be a more representative index than the CPI, chiefly because it reflects housing costs. The issue around suitability figured in a recent legal case, brought by telecoms firm BT, which wished to change uprating of pension payments from the RPI to the CPI on the basis that the former had ‘become inappropriate’. But the judge rejected BT’s claims, stating in his ruling that: ‘any index can do no more than provide an estimate of the increase in cost of living… it is impossible to say that RPI is wrong and CPI is right, or even that RPI is more wrong (or right) than CPI…’

The future for the different measures

IDR reports on the CPIH, CPI and RPI measures of inflation as part of our service to pay practitioners. We also survey them annually on their use of the respective statistics. But what is the future for each of the measures? The fact that the CPI excludes housing costs means that its use in uprating pay and benefits can feel unfair. The CPIH clearly represents an improvement in this regard. However, the rental equivalence approach has been criticised, on the grounds that owner-occupiers, by definition, do not pay rent, and therefore the CPIH indicator is failing to adequately measure what is happening to housing costs.

In addition, statisticians associated with the Royal Statistical Society have pointed out that the CPI and its variants, since they were designed for macroeconomic purposes, do not function as measures of inflation as it is experienced and perceived by households in their role as consumers. In line with this, they have proposed the development of a Household Inflation Index, different in several respects from the CPI/CPIH, that would remedy this shortcoming. As they highlight, their proposed measure’s ancestry can be traced back to the RPI and is a ‘return to the general principles underlying the RPI’.[1]

The ONS has responded to these developments by embarking on a programme of developing Household Costs Indices, initially as a complement to the existing suite of consumer price indices. Instead of a single index, though, based on costs for a ‘typical’ household, the ONS publishes the indices, which remain experimental, for different households – retired households, non-retired households, households with children and households without children. As such, the indices are unlikely to soon replace the current statistics in public usage.[2]

On the RPI, the recent House of Lords inquiry into its use found that despite the UK Statistics Authority (which oversees the work of the ONS in this respect) advocating against the use of the RPI, it remains in widespread use – for uprating corporate bonds, Government index-linked gilts, private sector pensions and in pay-setting, as well as the other uses referred to above. The Lords’ Economic Affairs Committee considers that the Authority’s position is untenable. It says: ‘the Authority should stop treating RPI as a legacy measure and resume a programme of periodic methodological improvements [to it].’ In addition, the Committee goes on to state that once the issue of how to capture owner-occupier housing costs has been settled, there should be a single general measure of inflation, to avoid ‘index-shopping’ and provide consumer and user confidence in this important economic statistic.[3] The Lords thought that this should be introduced within five years.

But the Government has reacted to the Lords' inquiry by announcing that the RPI is to be discontinued by 2030. The consultation over this prompted the Royal Statistical Society to host a debate on 21 July last year which heard sharp criticisms of the terms of the consultation, as well as defence of the Government’s position. For details of the proceedings, follow this link: https://rss.org.uk/news-publication/news-publications/2020/general-news/rss-open-meeting-on-rpi-–-event-report/

Some stakeholders are concerned that the Government is intentionally sidelining the RPI in favour of a measure that shows lower inflation, something that, if true, would at least accord with successive governments’ approach to inflation since the 1970s, which has been to maintain it at comparatively low levels. Whatever the truth of the Government’s objectives, the move has inspired new legal moves, this time by pension scheme trustees at BT, Ford and Marks & Spencer. The trustees are seeking a judicial review of the decision to ‘reformulate’ the RPI, which means that it will effectively become the same as the CPIH. The trustees say that the change would leave potentially millions of pensioners worse off as annual increases in their pensions would change from being based on the RPI to the usually lower CPIH. The outcome of the case will be important for the future of inflation statistics in the UK.

[1] ‘Towards a household inflation index: compiling a consumer price index with public credibility’, John Astin and Jill Leyland. See Astin-Leyland-HII-paper-Apr-2015.pdf (rss.org.uk)

[2] For more details see https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/householdcostsindices/preliminaryestimates2005to2017

[3] For details see the inquiry report here: House of Lords - Measuring Inflation - Economic Affairs Committee (parliament.uk) or Economic Affairs Committee Report: Measuring Inflation - House of Lords Library (parliament.uk)